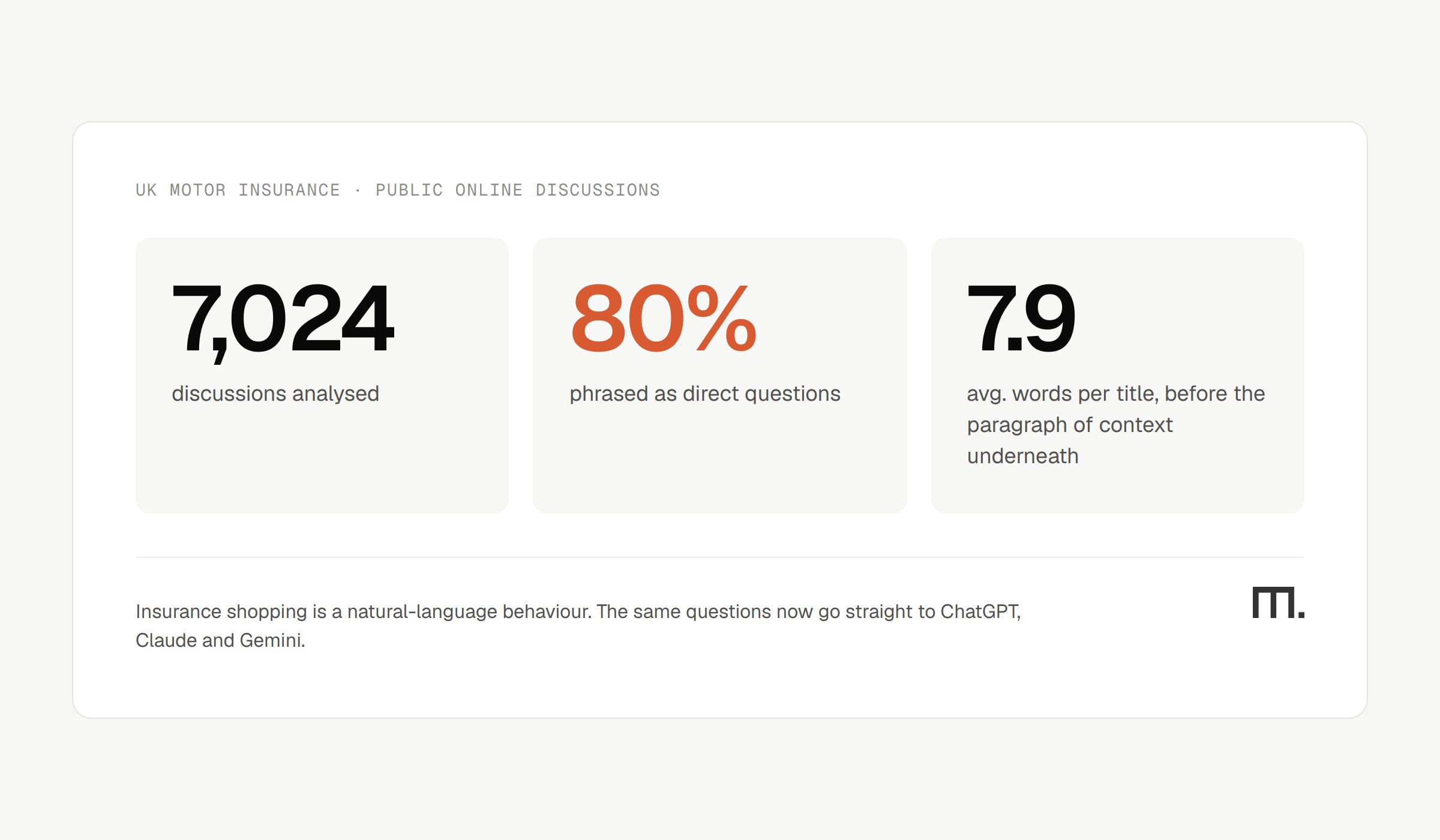

Roughly 80% of what UK drivers post about insurance in public online communities is a question, phrased in plain English, describing a specific personal situation. Not "compare motor insurance," but "can my son be a named driver if he's really the one driving the car most?" Those questions used to be answered by other people in a thread. Now they're answered, once, by an AI assistant, and for a growing share of shoppers that single answer is the last thing they read before they buy. This is the shift insurers need to plan for.

Where do insurance customers actually ask their questions?

For years, the smartest insurance marketers have quietly treated public discussion forums as a research channel. It's free, it's unfiltered, and it surfaces the questions customers would never put in a survey because they're slightly embarrassing, slightly confusing, or both. We analysed a corpus of more than 7,000 UK motor insurance discussions to map what people actually get stuck on. The pattern is consistent. Most insurer marketing is built around something else entirely.

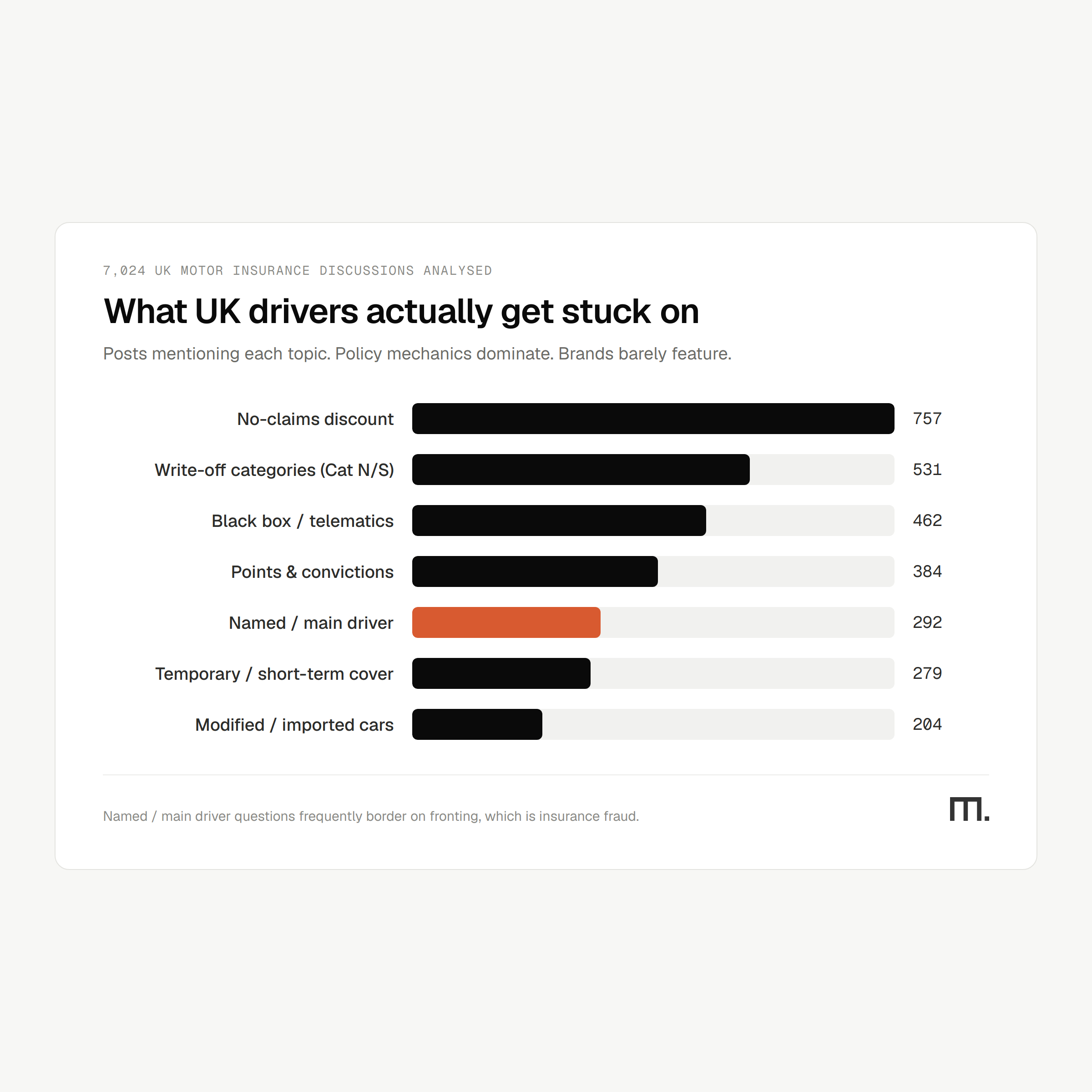

The most common car insurance questions from UK drivers are about policy mechanics, not brands. From 7,024 discussions analysed.

The questions are about policy mechanics. No-claims discount, write-off categories like Cat N and Cat S, black-box and telematics terms, points and convictions, named-versus-main-driver rules. These are the specific, high-stakes, easy-to-get-wrong details that decide whether someone buys the right cover or an expensive mistake.

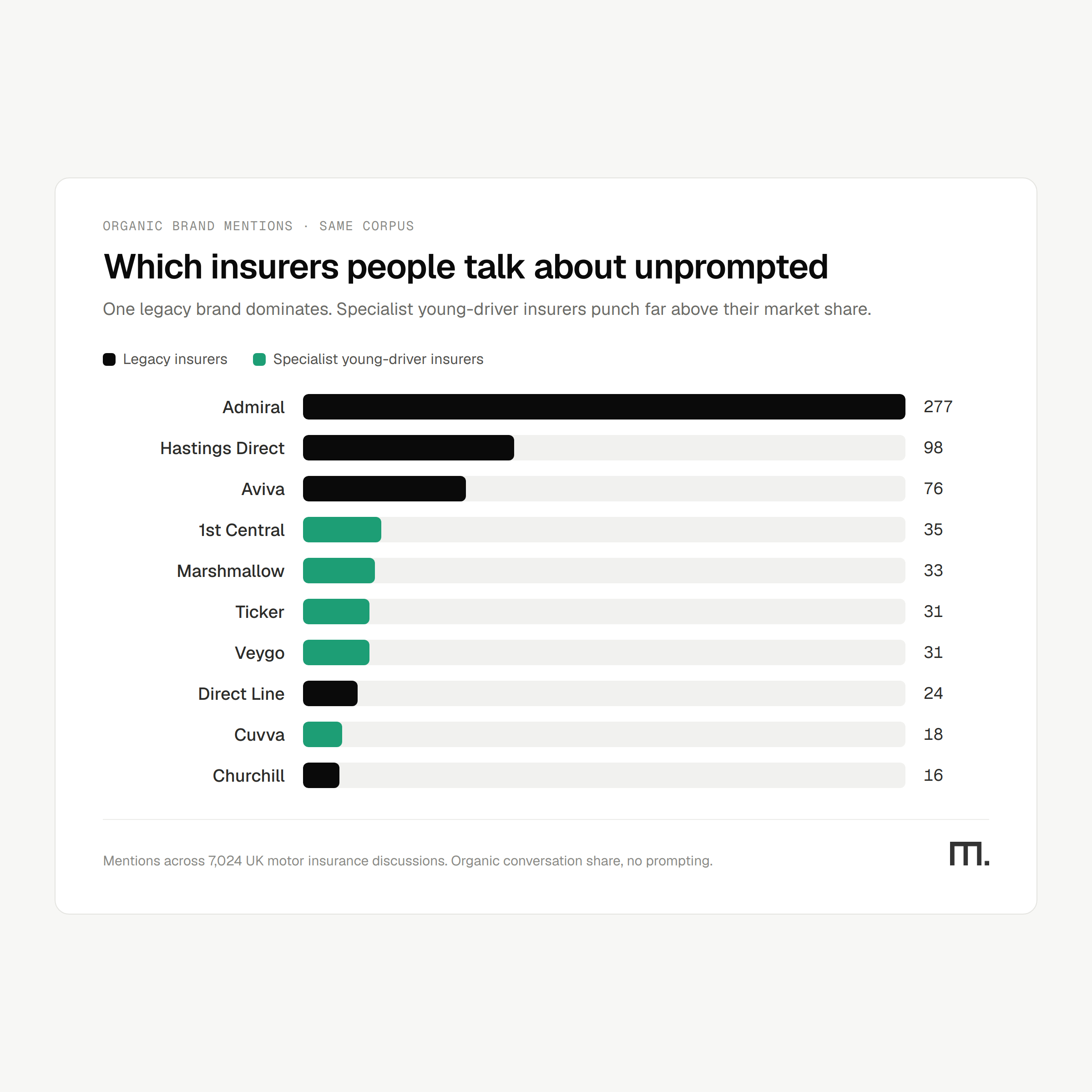

Admiral is mentioned nearly three times as often as any other insurer in organic UK motor insurance discussions.

Organic conversation concentrates on a small number of names. One legacy insurer is mentioned nearly three times as often as its nearest large rival, and a cluster of specialist young-driver insurers punch far above their market share, because they own the exact scenario, young and new drivers, that generates the most anxious questions.

And these are natural-language questions. Long, specific, situational. Seven or eight words in the title alone, and a paragraph of personal context underneath. That matters for what comes next.

Why is that goldmine moving from forums to LLMs?

The same questions, in the same messy, specific, human phrasing, are now typed directly into ChatGPT, Claude and Gemini. The behaviour hasn't changed. The surface has.

A forum gives you fifty replies, upvotes, corrections and counter-arguments. A large language model gives you one confident answer, with no thread underneath to catch it when it's wrong. When a model states the wrong excess figure, misdescribes how a no-claims discount transfers, or fails to flag that a "cheaper insurance" workaround is actually fronting (which is fraud), there is no crowd to correct it. For the shopper, that answer is simply the truth.

This is what Generative Engine Optimization measures, and why we built our UK insurer AI leaderboard: whether AI assistants name you, recommend you, and describe your cover accurately when a real customer asks a real question. The gaps are large, and they don't map neatly onto who wins in traditional search.

What happens when the customer is an AI agent, not a person?

Everything above is still the human-typing-into-a-chatbox phase. It's already reshaping distribution, and it's the on-ramp.

The destination is agentic: a person delegating a task to an AI that is authorised to act, and go and buy. Your calendar assistant renewing your travel cover before a trip. A household agent that quotes and binds car insurance when you change vehicles. This is a bet on where agentic AI is heading, and it's a reasonable one: the same platforms already surfacing insurance answers are the ones building agents that take actions.

When the buyer is software, the regulatory obligations do not disappear. Someone still has to ground every quote in real, live pricing rather than a plausible-sounding hallucination. Someone has to surface the right disclosures, enforce the conduct rules as the interaction happens, and keep a complete audit trail, whether the customer typed the question or delegated it to an agent. Retail rails were never built for that. Regulated products carry underwriting, disclosure, suitability and conduct duties that a generic "add to cart" flow simply ignores.

That's the layer Marrow builds. We sit between AI agents and insurer systems and do the hard part: turning a natural-language conversation, human or agent, into a compliant quote and a bound policy, grounded in your real pricing, with the disclosures surfaced and the audit trail intact. It's the same open standard, the AMI Standards, that lets any insurer be on the rail and any AI surface offer insurance through one integration.

The customers are already asking their questions in natural language. The only open question for insurers is whether the answer they get is accurate, compliant, and yours.

Original LinkedIn article here.

Frequently asked questions

What is Generative Engine Optimization for insurance?

Generative Engine Optimization, or GEO, is the practice of making sure a brand is named, recommended and accurately described when people ask AI assistants like ChatGPT, Claude and Gemini for recommendations. For insurers it means measuring and improving how models answer real customer questions about cover, which is a separate discipline from ranking in a Google search.

Why does it matter how AI assistants describe my insurance products?

Because for a growing share of shoppers, the AI's answer is the only answer they see before deciding. If a model misstates your excess, your cover terms or your eligibility rules, that error goes uncorrected and shapes the customer's decision. Accuracy in AI answers is becoming a distribution issue, not just a marketing one.

What is agent-mediated insurance?

Agent-mediated insurance is when an AI agent, acting on a person's behalf, requests quotes, compares cover and binds a policy, rather than the person filling in a form themselves. It requires a compliance layer that grounds quotes in real pricing, enforces conduct rules and keeps an audit trail, which is what the AMI Standards define and what Marrow provides.

Is fronting really fraud?

Yes. Fronting is naming an experienced driver as the main driver on a policy when a less experienced driver, usually a young or new driver, is actually the main user of the car. It understates the risk and the premium, which makes it a form of insurance fraud in the UK. If discovered, an insurer can void the policy and refuse to pay claims.

Marrow is the compliant infrastructure layer connecting AI agents to insurer pricing and underwriting systems, turning conversations into compliant insurance interactions. Get in touch to see how it works.